Parts of Spaceship Earth are Becoming Uninsurable

The rate of climate change surged alarmingly over the past decade, posing a ‘code red’ emergency for the world and the insurance industry.

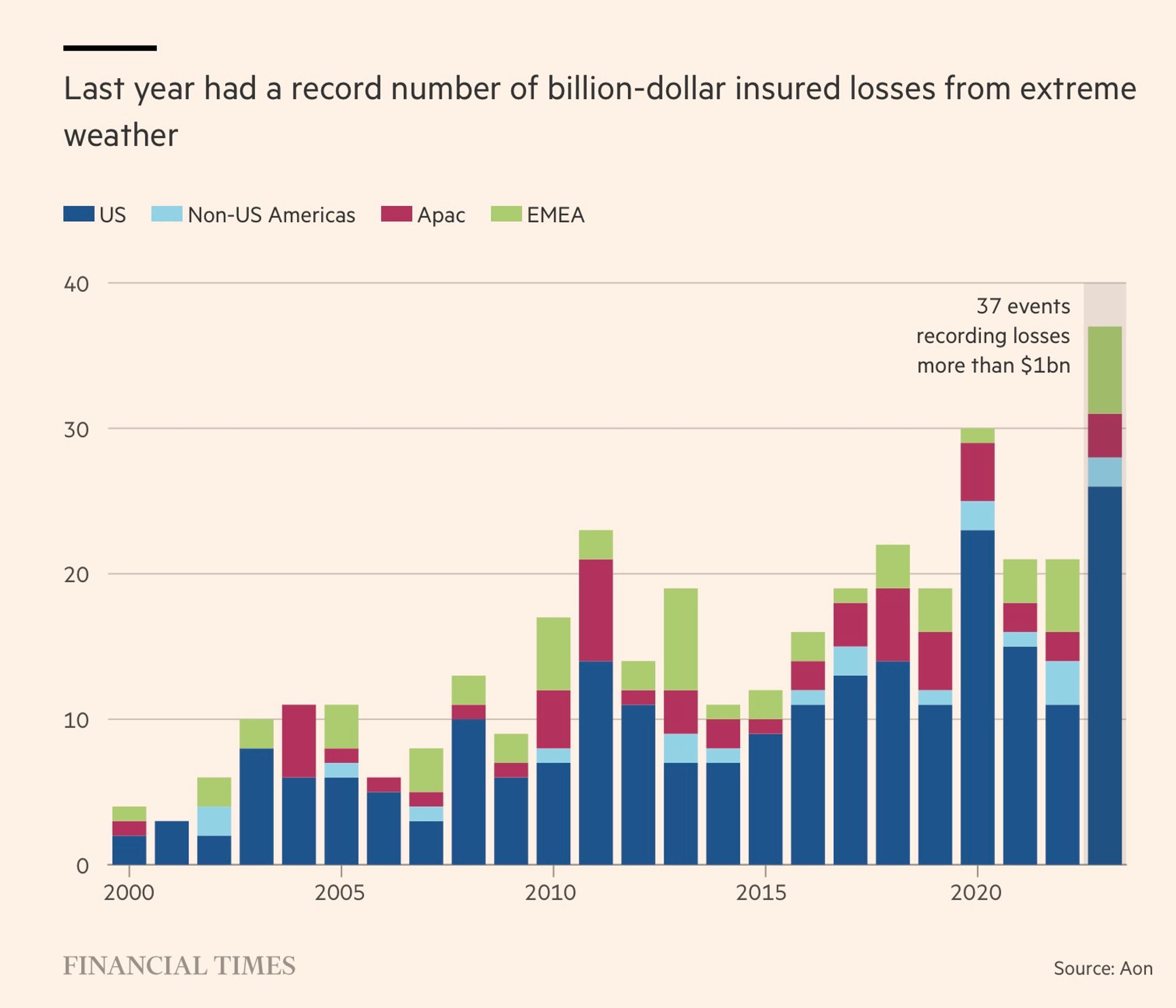

$122 billion total insured losses worldwide from weather-related natural catastrophes in 2023. (Swiss RE)

250% rise in economic losses over the past three decades due to climate change. (Capgemini)

60% of insurance risk managers “fear climate change is making certain geographic areas uninsurable.” (Financial Times)

About 40% of the US population lives in an area vulnerable to climate impacts including sea level rise, extreme weather and forest fires. How do we pay for the damages that occur and distribute the risk? This is a huge concern for the insurance industry in particular.

Ten insurers have gone belly up in Florida in just the last two years. Insurers are pulling back in risky areas, leaving state-backed insurance plans holding the bag. Both private and government-backed insurers are undercapitalized for dealing with the potentially massive disasters we will experience in coming years. This shortfall foreshadows more premium increases, and those increased premiums will not be paid only by those residing in higher-risk areas. Again looking at Florida as the canary in the coal mine, insurers have increased premiums across the state to cover their losses from Hurricane Ian.

Society and governance must change to address risks that insurers can no longer cover on their own. Collaboration is key to meeting this challenge. A really important part of it, and a piece that can be difficult, is developing new partnerships across sectors. Can we get the public (local, state and federal government agencies), private (insurers and reinsurers), non-profits (charitable organizations designed to deliver aid after a catastrophe) sectors, and homeowners/insureds working together to solve these problems?

Crew consciousness refers to the idea that humans are all active crew members on Spaceship Earth… not passive passengers, and have a shared responsibility to address global challenges like our climate crisis.

All Hands on Deck

People across society are growing skeptical of business as usual. They see that what used to work is no longer up to the task. Crew consciousness dictates that we are all in this together and must work collaboratively to address the challenges facing humanity. It suggests that we need to shift from a mindset of individualism to one of collective responsibility and action.

Crew consciousness could be applied in a number of ways as the insurance industry struggles to adequately address the risks, impacts and opportunities inherent in our climate crisis. Human and environmental systems are interconnected. Our climate crisis affects not only physical assets but also the well-being and livelihoods of individuals and communities.

Traditional insurance models, which primarily focus on monetary compensation for physical damages, do not adequately address the complexities of climate change. A more holistic approach, that incorporates crew consciousness, would involve not only compensating for tangible losses but also nurturing a sense of responsibility and accountability for sustainable practices. By integrating crew consciousness into insurance business models, individuals and organizations could be encouraged to adopt environmentally friendly behaviors and support initiatives aimed at mitigating climate change.

Is a staid, venerable and risk averse industry able to make the systemic changes necessary to meet the challenges of today’s world? Insurers are well aware of what’s happening. They have the data. They see that claims are increasing in size and frequency as the impacts of climate change have grown year over year for the past 30 years or so. They see the trends. They know their current business practices cannot meet the challenges.

Companies actively engaged in eco-friendly initiatives might receive reduced premiums, while those contributing to climate change could face higher costs. The insurance industry should collaborate with scientific communities and policymakers to develop risk assessment models that incorporate climate change projections. By using advanced data analysis and predictive modeling, insurers could better anticipate the potential impacts of climate change on various sectors and adjust their coverage and premiums accordingly.

The insurance industry should evolve beyond traditional monetary compensation and actively encourage regenerative practices through the integration of crew consciousness. What if a collaboration of public and private actors joined the insurance industry in promoting and delivering climate literacy through the lens of crew consciousness? By adopting this approach, the industry could contribute to the collective effort in combating climate change and protect the well-being of people and nature.

The insurance industry needs to make drastic changes in order to meet the challenges of our climate crisis. It needs to engineer and promote climate resilience practices. Here are some ideas:

- Collective Risk: Climate change presents significant risks that affect the entire planet and all its inhabitants. Insurers can adopt a crew consciousness perspective by recognizing the interconnectedness of these risks and developing collaborative solutions to mitigate them.

- Shared Responsibility: Insuring against climate change impacts requires acknowledging that the responsibility should not solely fall on individual policyholders. Insurers can play a role in fostering crew consciousness by promoting regenerative practices, encouraging climate-friendly behavior, and supporting initiatives that mitigate climate risks.

- Innovative Coverage: Insurers can develop new insurance products tailored to address the specific risks associated with the climate change impacts each individual insured is likely to experience. This could include coverages for extreme weather events, rising sea levels, droughts, wildfires, or other climate-related risks… and will need to be highly customized. The development of innovative policies can be guided by a crew consciousness mindset, focusing on collective well-being and long-term sustainability.

- Collaboration and Partnerships: Insurers can collaborate with various stakeholders including governments, scientists, environmental organizations and communities, to share knowledge, data and resources. This collaborative approach can help assess risks accurately, develop effective risk models, and implement preventive measures.

- Education and Awareness: Promoting crew consciousness within the insurance industry involves raising awareness among policyholders, employees and other stakeholders. Insurers can educate their clients about the importance of climate change mitigation, sustainable practices, and the benefits of environmentally conscious behavior.

- New Services: Property & Casualty and Reinsurers are already training their actuaries, underwriters and claims adjusters on climate risk management and adaptation practices. Why not extend that to policy holders? Policy holders who complete the training and devise (with help from the company) individual climate risk adaptation plans would earn premium reductions.

Crew consciousness can be the lever the insurance industry uses to move from a reactive stance (wait until disaster occurs and then pay out damages) to a proactive stance (here’s how we safeguard your property, livelihood and lives!) against climate impacts.

The industry is already moving in this direction, but the moves need to be bolder, faster and reach beyond the borders of the company itself.